{kind=link}

Are cooling measures beneficial or detrimental?

In the early stages of our real estate market, we faced huge downturns during the Asian Financial Crisis (1997), DotCom burst/SARS (2000) and Global Financial Crisis (2008). In those days, there were no regulating policies such as Total Debt Servicing Ratio (TDSR), Additional Buyer Stamp Duty (ABSD) and 10% of downpayment is sufficient enough to get a 90% loan.

As a result, people tend to over-leverage. Market speculation was rampant at that point of time. When a financial crisis hits, people are not able to keep up and they let off their properties quickly to cover their losses. That was how the market experience major declines during times of financial crisis.

Fast forward to 2009, the market has boomed upwards with a 62.2% increase in our private property index. With the government’s effort to moderate the market, there were 9 cooling measure in place during that period of time. Specifically in 2013, TDSR was implemented which cooled the market for the next 4 years.

2017 Onwards, our market has moved upwards gradually, unaffected by subsequent cooling measures and the Pandemic. With the cooling measures in place, speculation has been significantly reduced. Also, with TDSR buyers practise a prudent behaviour on leveraging. This provides buyers a safety buffer in times of a financial crisis. As such our market remains resilient during the 2018 cooling measures and Covid-19.

The cooling measures have formed a strong foundation in our property market, to curb against speculation and rising price inflation. Thou, it is common to hear people say that Singapore’s market is heavily controlled which brought dismay to many. Should Singapore release the cooling measures, allowing prices to inflate much further and foreigners or the wealthy to own more property in the market. How will it affect the rest of us?

Nicholas Lim

Cooling measures mentioned:

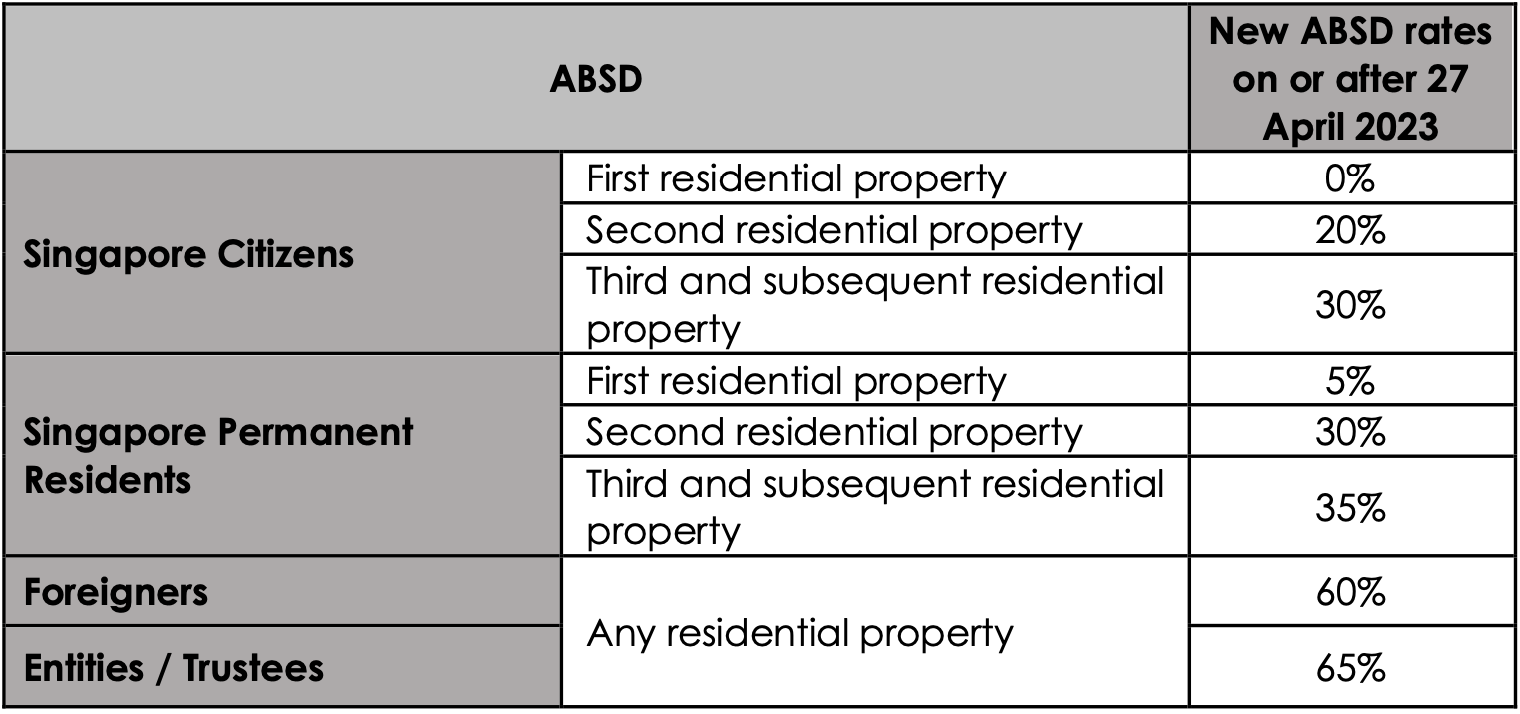

Additional Buyer Stamp Duty (ABSD)

ABSD incurs a tax on different group of buyers depending on their number of properties own at the time of purchase. The ABSD’s primary purpose is to deter speculative buying, which can lead to artificial inflation in property prices. This measure is particularly targeted at cooling the demand from certain segments of buyers, such as investors and foreigners, thereby ensuring a sustainable property market conducive to genuine home buyers.

Total Debt Servicing Ratio (TDSR)

Housing Loans were capped at 60% in 2013, it was later revised to 55% in 2021. This is a measure to prevent homebuyers from borrowing more than what they could afford.

E.g. Person A has an income of $10,000SGD. He is restricted to use only $5,500SGD to pay for all of his loans including mortgage.